If you really want to know what a society truly values, ignore its speeches and examine its balance sheets. Moral arguments might shape the slogans; capital rules shape the behaviour.

That’s why the Bank of England’s latest climate move matters far beyond London. With its new climate risk standards for banks and insurers, the central bank has effectively pulled climate out of the cosy world of sustainability reports and dropped it into the hard core of prudential regulation. Climate risk is no longer a public relations issue in the UK. It’s now treated, formally, as a question of safety and survival for financial institutions.

On the surface this looks like a technical shift: new expectations for boards, fresh guidance on scenario analysis, more stringent integration into capital planning. But underneath lies something more revealing. The financial system is being forced – reluctantly and partially – to admit that “the economy” does not float above the biosphere. It’s embedded in it. Damage the latter enough, and the former loses its foundations.

The more interesting story is what this tells us about a civilisation still trying to handle an existential predicament as if it were just another category of risk.

Climate Leaves the Marketing Brochure and Enters the Boardroom

For the past decade, climate has been handled primarily as optics. Banks and insurers announced net-zero commitments, wrote glossy sustainability sections in their annual reports, and hired ESG teams tasked with producing ever more elaborate diagrams. Climate sat in its own little annex – adjacent to strategy, but never quite allowed to govern it.

Those days are ending. The Bank of England now expects boards and executive teams to treat climate change in the same way they treat credit risk, liquidity or solvency. It must show up in risk appetite statements, decision-making, business plans and capital models. Board members can no longer point vaguely to a sustainability officer somewhere down the corridor. They are personally answerable for how climate risk is understood and managed across the institution.

There is no new grandstanding role – no “Chief Climate Czar” to soak up responsibility. Instead, climate is being threaded through the responsibilities that already exist. Risk officers, finance directors, business line heads: all of them are now on the hook. If climate risk is mishandled, regulators will not just wag fingers; they can tighten capital requirements, cap certain activities, or escalate supervisory intervention.

The underlying message is blunt: neglect climate, pay more for capital. Ignore climate, expect governance questions. Pretend climate is someone else’s problem, and you become the problem.

Scenarios That Actually Bite

For years, climate scenario analysis was the regulatory equivalent of a school project. Institutions dutifully produced charts showing different 2050 temperature pathways, took part in exploratory exercises, and then quietly returned to business as usual. The scenarios had little bearing on which clients they financed, what products they designed, or how they set prices.

The new regime is designed to break that habit. Scenarios are no longer a decorative appendix. Boards must now define why they are running them, what decisions they will inform, and how the findings will be used. Capital planning, stress testing, risk appetite, product development, even the choice of markets to enter or exit – all are meant to be influenced by those climate futures.

Crucially, firms are told to err on the side of caution when data are patchy or models uncertain. They are expected to use conservative assumptions rather than hiding behind gaps in knowledge. The old defence – “we don’t have enough data yet, so we can’t act” – is being dismantled. This changes the role of scenario analysis completely. It’s no longer theatre or window dressing. It becomes a governance weapon:

· What does your mortgage book look like if a coastal region floods every few years and insurance quietly pulls back?

· What happens to your agricultural loans when heatwaves and droughts turn from anomalies into routine features of the growing season?

· What does your life portfolio look like if mortality and morbidity patterns shift under sustained climate stress?

These are not footnotes in a model. They are questions about whose homes are still habitable, whose livelihoods remain intact, whose communities will be quietly written off as unviable. When many institutions act on such scenarios simultaneously, they don’t simply “anticipate” the future. They help shape it, deciding which geographies and sectors are backed, and which are left to fend for themselves.

No More Hiding Behind the Data

Modern finance has trained itself to believe that once enough numbers are collected, risk can be tamed. Climate chaos exposes the vanity of that belief. We’re dealing with feedback loops, tipping points and systemic shocks that do not behave nicely. They don’t respect confidence intervals. Rather than waiting for perfect metrics, the new expectations tell firms to map their data gaps, admit their blind spots, and then move anyway. Use prudent interpretations. Make defensible judgements. Be able to explain them.

That might sound dry, but it cuts into a much deeper assumption that powers industrial economism: the default right to act first and apologise later, on the grounds that “we didn’t know”. With climate, regulators are signalling that not knowing is no longer a free pass. You are expected to know enough to be cautious. Whether that leads to genuinely cautious behaviour or to formulaic overlays bolted onto unchanged business models is still an open question. Supervisors can demand prudence in process; they cannot guarantee courage in substance.

A Global Drift, with Fractures

This is not a uniquely British drama. Around the world, consensus is quietly forming among central banks, supervisors and global standard‑setters that climate is no longer an optional ethical add‑on but a straightforward matter of financial stability. The language has shifted: from sustainable finance as a niche, to climate risk as something that must be woven into existing risk categories, disclosure obligations, data systems and supervisory tools.

The picture is far from uniform. Some authorities are moving in the same direction as the Bank of England – asking, in effect, how climate risk feeds into capital planning and governance, and what happens if it’s ignored. Others, under political pressure, are rowing back, insisting that existing generic rules are enough and that no explicit climate framework is required.

Still others sit in a transitional zone: engaging in climate scenario exercises, building data platforms, issuing high‑level principles, but hesitating to tie those efforts to hard consequences for banks and insurers. In many of these jurisdictions, climate vulnerability is not a future abstraction but a lived experience in coastal property, agriculture, energy systems or health. The unresolved issue is whether supervisors will allow their prudential rules to touch those pressure points, even when that exposes uncomfortable truths about current development models.

We are, in other words, watching a global drift towards climate‑aware prudential thinking, marked by bursts of acceleration and episodes of denial. The deeper pattern is clear enough: wherever regulators accept that climate risk can destabilise balance sheets, the logic pulls them towards the same conclusion – climate belongs in the prudential spine, not in a marketing brochure. The resistance is not about the physics. It is about the politics of what follows once that conclusion is conceded.

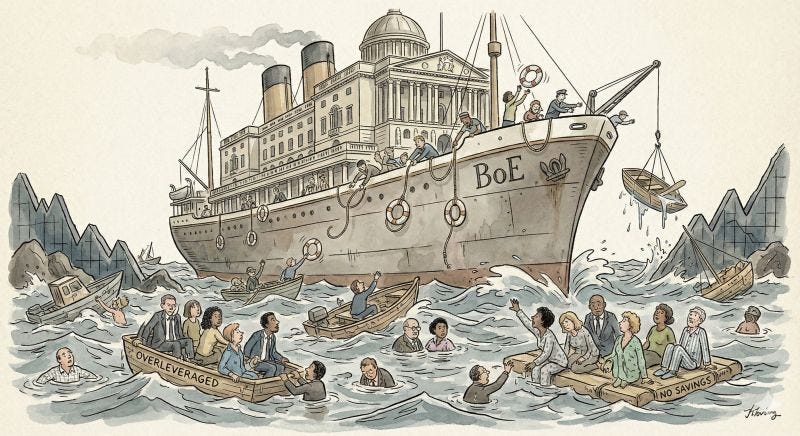

When Insurers Retreat, Banks Hold the Bag

One of the more far-sighted aspects of the UK’s new climate framework is the explicit recognition that banks and insurers are entangled in a single feedback system. As climate-related disasters multiply – floods, wildfires, storms, crop failures – insurers face rising claims and more volatile loss patterns. In response, they can raise premiums, tighten terms, or simply withdraw from high-risk areas and sectors. We can already see this in parts of the world where home insurance has become unavailable or unaffordable.

Yet risk doesn’t evaporate simply because an insurer steps back. It migrates. A house that cannot be insured is still a house; its owner may still have a mortgage. The bank now finds itself exposed to an asset that could be physically damaged and financially impaired, with little warning. Multiply that across thousands of properties in a floodplain, or across energy-intensive firms exposed to abrupt policy shifts, and the transfer of risk from insurer to bank becomes systemic. Regulators are now insisting that banks trace those lines of contagion. They must track where insurance coverage is thinning out, where premiums are spiralling, where exclusions are becoming the norm. Insurers, in turn, are expected to understand how their underwriting and pricing decisions affect lending, investment and broader financial stability.

Looked at through a wider lens, what comes into view is an architecture that has spent decades perfecting the art of shifting risk onto those with the least power. When insurers withdraw and banks tighten credit, who is left carrying the risk? Households on low incomes. Farmers without alternatives. Informal workers without savings. Small enterprises that cannot simply move to “safer” jurisdictions. So while the central bank talks about prudential soundness, a harsher reality is emerging in parallel: a world in which solvency for large institutions can coexist with growing precarity for those they no longer deem bankable or insurable.

The “Learning Phase” Is Over

For a long time, climate risk in finance was treated like a training exercise. Supervisors encouraged experimentation, pilot projects, voluntary disclosures, capability-building. Firms could dabble in climate modelling, publish some scenarios, and reassure themselves that they were “on the journey”. That indulgent period is now closing. The new standards are in force. Institutions are expected to review their current state, draw up action plans in the near term, and have climate risk fully embedded into capital processes and risk management systems within the next couple of years. Supervisory intensity will step up accordingly.

This shift does two things at once. On one level, it acknowledges the obvious: climate risk is not something that might arrive one day. It’s already here – in catastrophic losses, in supply chain disruptions, in heatwaves that damage labour productivity, in policy uncertainty around carbon-intensive industries. On another level, it risks creating the impression that once climate is “integrated” by a certain date, the job is largely done. Tick the box. Embed the model. Move on.

But the physical world is not working to regulatory deadlines. Climate disruption will continue to accelerate. New feedbacks will surface. Regions once thought relatively safe will be hit. Social tensions over loss and damage will intensify. If climate risk becomes just another column in a risk dashboard – managed with the same routines and assumptions that helped generate the problem in the first place – then we will have achieved better reporting, not better futures. The ritual will have been updated; the worldview will remain untouched.

The Worldview Hiding Inside the Rulebook

Behind all these technical changes sits a deeper story about fundamental beliefs. Prudential regulation rests on an implicit picture of how the world works: that growth is normal, that financial returns can compound indefinitely, that the biosphere is a backdrop to a human economic drama rather than its host, and that risk can be sliced, priced and spread so that it becomes tolerable.

Climate breakdown punctures that picture. If crops fail across multiple breadbaskets at once, if major cities face recurrent flooding, if heatwaves push health systems to the brink, the idea of a neatly “resilient” financial sector starts to look like self-deception. You can’t have a thriving banking system perched on top of widespread ecological collapse and social breakdown indefinitely. Sooner or later the losses migrate upwards.

Regulators are now insisting that banks and insurers “own” their climate risk. That’s an important advance on treating climate as a charitable side issue. But it stops short of addressing a far more uncomfortable question: is the current financial framework – addicted to leveraged growth, debt-fuelled consumption and fossil energy – fundamentally compatible with a habitable planet? Or, sharpened still further: can rules designed to stabilise a destructive system be repurposed to transform it, or will they always default to protecting incumbents?

At present, the new climate regime still speaks the language of risk mitigation, not systems redesign. Yet by compelling institutions to look more honestly at what climate disruption means for their own survival, it opens up a crack. Once you see that your business model depends on conditions that are rapidly vanishing, how long can you pretend that a few tweaks to risk weights will suffice?

Proportionality, and the Comforting Fiction of Safety

The Bank of England insists that its expectations will be applied proportionately. A small local building society or mutual will not be expected to develop the same analytical machinery as a global investment bank. On paper, this is sensible. Capacity and complexity differ. Climate, however, does not scale politely. A single flood can bring down a small insurer. A prolonged drought can devastate a regional bank whose loan book is concentrated in agriculture. A sequence of storms can erode the capital of local institutions that anchor entire communities. Proportionality, if used as an excuse for lower vigilance, can easily turn into complacency. It can reinforce the illusion that climate risk is primarily the concern of “big players” and complex groups, and that simpler institutions can afford to be relaxed.

This connects to another acute issue: what do we now mean by “safety”? Regulatory language still suggests that risk can be identified, measured, and contained within acceptable limits. Yet climate operates through thresholds and cascades that don’t respect those limits. In a world of intensifying climatic instability, is it honest for any institution to claim that it is safe in an absolute sense? Or are we really talking about relative safety – safer than others, for now?

If safety becomes relative, then prudential success for one set of firms can coexist quite easily with systemic failure for millions of people. From a regulatory vantage point, the system might be “sound”. From the vantage point of a farmer whose land has become unviable or a coastal family whose home is repeatedly inundated, it is anything but.

Climate Risk as a Mirror, Not Just a Metric

Interpreted narrowly, the Bank of England’s move is about making risk systems more accurate: better governance, better scenarios, better data handling, better capital planning. Necessary work, but still operating within the same mental architecture that gave us escalating environmental breakdown in the first place. Interpreted more broadly, it’s an invitation – albeit not an intentional one – to use climate risk as a mirror. That mirror reflects back the operating system of contemporary civilisation: a world-system built on extraction from ecosystems and from human labour; a belief that technology and markets can always outrun biophysical limits; a willingness to treat the most vulnerable as shock absorbers for elite misjudgement.

When financial institutions are forced to map what a warmer, more volatile planet does to their portfolios, they are not just analysing risk. They are encountering the consequences of the worldview they have helped entrench. At that point, several possibilities arise.

One path is retreat. Institutions do what is required to satisfy supervisors: they improve their models, adjust their capital, shift exposures, and carry on more or less as before. Climate damage increases. The system responds by pricing it more smartly and diverting it away from those with bargaining power. Risk becomes more “efficiently” allocated; harm becomes more concentrated.

Another path is inquiry. Some boards and executives, facing the implications of their own scenarios, may start asking a different order of question: If continuing to fund high-emissions activities drives our own future losses, why do we cling to those activities? If large segments of society and entire regions are drifting into uninsurability, what kind of economy are we sustaining? If our models insist that certain futures are filled with widespread loss and displacement, why are we content to prepare for them rather than change course?

Those questions sit at the intersection of ethics, strategy and survival. They are not confined to any one country. A community banker in Bangladesh, a regulator in Kenya, an insurer in Brazil, a pension fund in Germany – all are now operating within the same emergent pattern: a financial world-system rubbing up against planetary constraints it has long dismissed as externalities.

Towards a Different Notion of Prudence

In the conventional prudential playbook, prudence means protecting capital, keeping ratios within bounds, and demonstrating that your institution can withstand plausible shocks. That’s the lens through which climate is now being pulled into the regulatory mainstream. But for a family in a low-lying island nation, prudence means having a home that will still be there in ten years. For a nurse in a city where heatwaves are becoming deadly, prudence means a health system that can cope. For a smallholder farmer, it means water and soil that can sustain crops through erratic seasons. These are not sentimental concerns; they are the foundation on which any financial system that claims legitimacy must rest. As climate disruption deepens, the gap between prudence-as-capital-preservation and prudence-as-life-preservation will only widen unless we consciously bring them together.

The Bank of England’s new climate rules can be read as a small move in that direction. They acknowledge, implicitly, that the financial balance sheet and the planetary balance sheet are converging. Losses in one bleed inexorably into the other. Yet the hierarchy remains inverted. The primary question is still: How does climate risk threaten banks and insurers, and what must they do to protect themselves? A more radical reframing would start elsewhere: How might banking and insurance be reimagined so that they actively help stabilise the climate and support equitable, resilient livelihoods?

That reframing is not on the official agenda—yet. But by pushing climate risk into the very heart of prudential practice, regulators have set in motion a chain reaction. Institutions everywhere will be forced into a more honest confrontation with the world their balance sheets presuppose. What we make of that confrontation – whether we use it merely to survive a little longer, or to change far more deeply – remains an open, and still live, choice.